Automation in the delivery/logistic and warehousing/fulfilment chain is a growing market. A particularly exciting subset of this is the use of mobile robots, drones, and autonomous vehicles for automation of movement-based tasks. This field encompasses a diverse range of robots, drones, and autonomous vehicles, which help goods in their journey from origin to destination (see below).

Our report "Mobile Robots, Autonomous Vehicles, and Drones in Logistics, Warehousing, and Delivery 2020-2040" finds that the market for mobile robotics and drones in delivery and warehousing is likely to reach a staggering $81 and $290 Billion in 2030 and 2040, respectively. Of course, the devil is in the detail and this headline figure masks great diversity of technologies, markets, form factors, and fortunes.

In the rest of this article, we draw from our updated report to highlight the key trends in the use of mobile robots, drones, and autonomous vehicles in this sector. In this article, we focus on the use of mobile robots and autonomous vehicles in indoor applications. In a follow-up article, we focus on outdoor applications.

The report "Mobile Robots, Autonomous Vehicles, and Drones in Logistics, Warehousing, and Delivery 2020-2040" provides a comprehensive analysis of all the key players, technologies, and markets. It covers automated as well as autonomous carts and robots, automated goods-to-person robots, autonomous and collaborative robots, delivery robots, mobile picking robots, autonomous material handling vehicles such as tuggers and forklifts, autonomous trucks, vans, and last mile delivery robots and drones. For more information please visit www.IDTechEx.com/Mobile.

These shows pictures of products and prototypes of various mobile robots and ground-based autonomous vehicles aimed at automating a part of the warehousing and delivery chain. These images, which exclude drones, are, in no particular order, from the following companies: Amazon, Geek Plus, GreyOrange, Flashhold (Quicktron), HIK Vision, Scallog, Eiratech, Hitachi , TuSimple, embark, Starsky, Ike, Einride, Kodiak, PlusAI, Fabu, Daimler, Waymo, Hyundai, Baidu, SeeGrid, Geek Plus, Baylo, Vena Technologies, Kollmorgen, HIK Vision, AutoGuide (Teredyne), RoboCV, Knapp, Omron Adept Mobile Robotics, Mobile Industrial Robots (Teredyne), Locus Robotics, Canvas Technologies (Amazon), 6 River (Shopify), Otto Motors, Fetch Robotics, InclubedIT, DroneFutureAviation, Zhen Robotics, Meituan-Dianping, ZMP, Alibaba, Continental, Segway, Refraction, TwinWheel, Robby Technology, Amazon, Dispach (Amazon?), KiwiBot, JD, TeleRetail, Toyota, Neolix, Nuro, Ford, Gatik, etc.

To learn more about these products please visit www.IDTechEx.com/mobile

Indoor automation

e-commerce is changing the way warehouses are constructed and operated. One way or another, warehouses must become more adept and efficient in handling multi-item instant order fulfilment. The use of automation is an essential part of the answer to this requirement.

Automated guide carts and vehicles (AGC and AGV) have long been in use. They are infrastructure dependent, meaning that they follow a fixed infrastructure, such as conductive wire or magnetic tape, in going from A to B. Therefore, they are reliable and trusted to handle all manner of payloads. Their installation is however time-consuming, and their workflow is difficult to adapt. Furthermore, they, in their classical forms, are neither fast nor efficient utilizers of space. Finally, they do not lend themselves to human-robot collaborative workflows.

Consequently, as a technology, we think that they are on shaky ground, unless they adapt. This is because the technology is evolving towards more autonomous and infrastructure-independent navigation. We forecast that they will tend towards obsolescence and increasingly become confused to ever narrower market niches. Overall, our report "Mobile Robots, Autonomous Vehicles, and Drones in Logistics, Warehousing, and Delivery 2020-2040" finds that their market will shrink by 50% in 2030 compared to the 2019 level.

In many supplier quarters, adaptation is underway. However, many will find the journey too challenging given that that the emerging technology will require software expertise. Bridging the skills and knowhow gap and evolving the product portfolio will not be straightforward. Indeed, it poses challenging strategic questions in terms of how to acquire the necessary knowhow.

A bright spot for automated robots

One very bright spot for automated robots however is in goods-to-person automation within fulfilment centres. Special robot-only zones are created within warehouses in which these robot fleets move racks at high speeds to a manner picking station. The productivity gains are clear and proven. The technology results in space-efficient and compact warehouses. The pick-rates significantly improve and the headcount drops.

Many product design innovations helped enable this market. The hardware requires good acceleration and deacceleration to operate at high speeds with minimal spillage. The racks require special adaptations to steady the load during transit. The suspension system- which lifts and lowers the racks- require special design and engineering. The robots will include multiple motors, allowing them many degrees of freedom in movement. The navigation technology itself is not complex though as it is often fiducial based, mainly in the form of barcodes often printed at regular intervals on the ground.

They key value-add technologies are on the software side though. This includes the entire stack from customized firmware sitting on the motor drivers all the way to the fleet and task management levels. The business model is also an important differentiator with many moving towards becoming full solution providers.

This is a fast-growing market space. The landscape was set on fire when Amazon acquired Kiva Systems for $775M in 2012, thereby leaving a gap on the market. Today, significant well-funded alternatives such as GeekPlus (389$M), GreyOrange (170$M), and HIK Vision ($6Bn revenue) have emerged, achieving promising and growing deployment figures. The number of start-ups has also increased, especially around within the 2015-2017 period. Not all will be successful though even if they offer a good enough technology. In particular, doubts over the long-term viability of some start-ups' business model and financial health acts a barrier against long-term adoption by major end users.

We forecast the annual unit sales to double within 6 years. Despite the large deployments already, we assess the real global inflection point to arrive around 2024 beyond which point the pace of deployment will dramatically accelerate. Indeed, our report forecasts that between 2020 and 2030, more than 1 million such robots will be sold accumulatively. It is therefore an exciting time. To learn more please visit www.IDTechEx.com/Mobile.

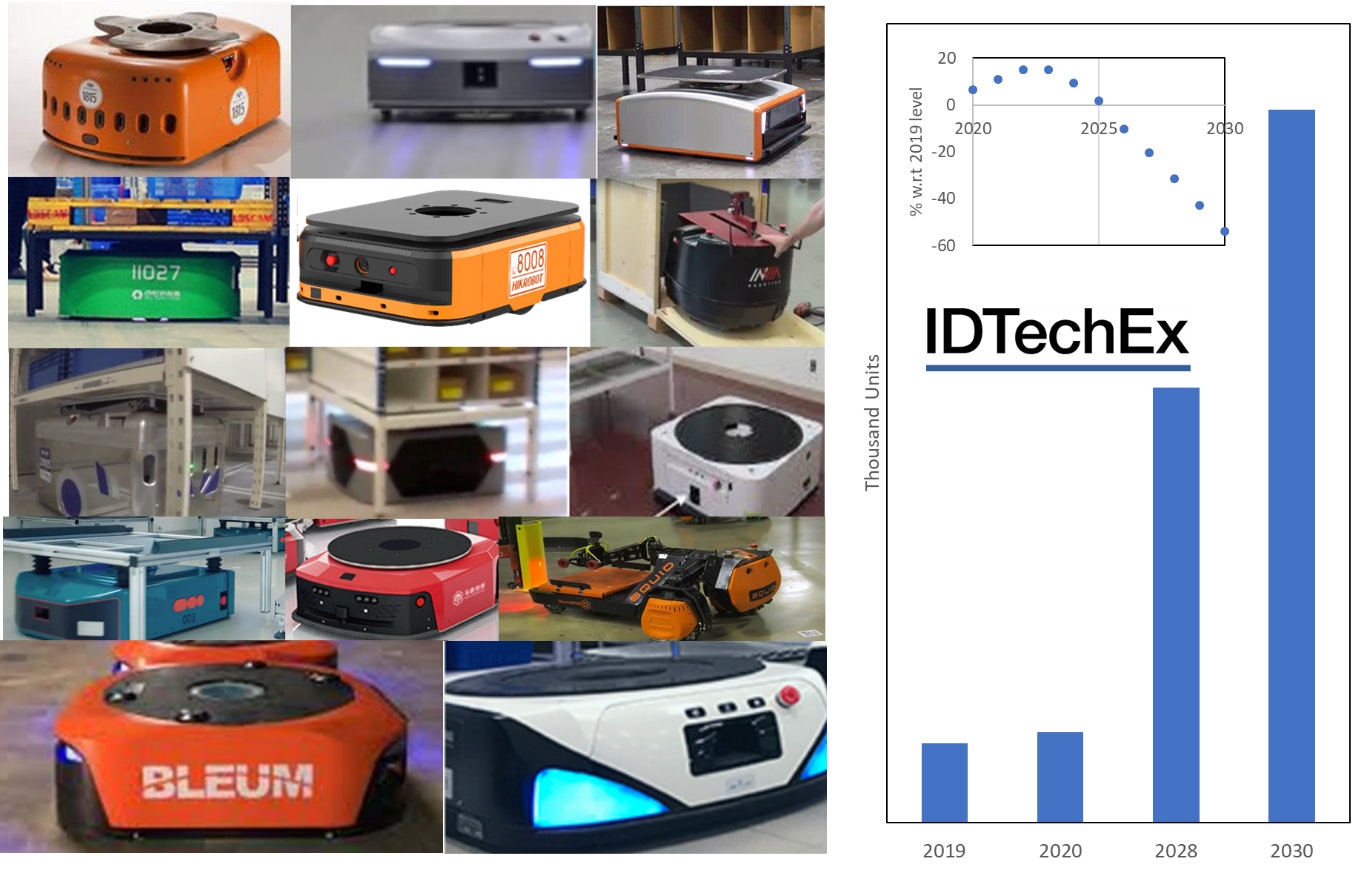

The images on the left show various examples of goods-to-person robots. Almost all have fiducial-based navigation, e.g., barcode following. They have nearly the same approach. The odd-one-out from this particular collection is InVia Technology which can be used in existing infrastructure due to its pick-up mechanism. The products shown here are from the following companies: Amazon, Geek Plus, GreyOrange, Flashhold (Quicktron), HIK Vision, Scallog, Eiratech, Hitachi, Myrmex, Malu Innovation, Bionic HIVE, Beijing Ares Robot Technology Co, and Prime Robotics (formerly Bleum Robotics). In this image, we have excluded robots used in ASRS systems from the likes of AutoStore, Ocado, Exotec Solutions, and so on. The forecast figure on the right shows the near-term forecast for these goods-to-person robots. The deployment numbers are fast increasing. Our projections in the report extend until 2040. The forecast model considers the rate of growth of the addressable market by considering the growth in fulfilment centres, the size of these centres, and the number of robots deployed per area. Furthermore, our model builds reasonable scenario considering the penetration of these technology into this field. The inset shows the decline of the traditional infrastructure dependent automated guided carts. The figure shows the rate of change w.r.t to the value in 2019. To learn more, please visit www.IDTechEx.com/Mobile.

Towards autonomous indoor robots and vehicles

The outlook for classic AGV/AGCs do not look bright. A major reason is that the navigation technology is transitioning from automated to autonomous. The primary benefit is that the navigation becomes infrastructure independent, allowing the workflow to be easily modified. The autonomous mobility also allows various modes of collaborative workflows between robots and humans, thus extending the utility of such autonomous mobile robots and vehicles to existing facilities.

The technology is enabled by better SLAM algorithms. The algorithms - based on different sensors including stereo camera and 2D lidars - are evolved enough to handle safe autonomous navigation within many structured indoor environments with high degree of control and predictability. These robots are easy to install and to train.

The technology options however are still many, and choices have long-lasting strategic consequences. A common process is to use 2D lidars to develop a map of the facilities during the training phase, e.g., walking the robot around the facilities. The fixed reference objects will be marked during the set-up phase. This system is fairly simple. However, it does not deal well with dynamic and changing environments. Another approach is to use camera vision and deep learning to also identify and classify objects. This is computationally more complex, but will enable a more flexible system that can have more intelligent decision making in complex and changing environment. It extends the utility of such vehicles to more indoor scenarios and allows a mobile robot that intelligently responds to its changing environment.

The business models are also various and evolving. Some are offering their technology as RaaS (robot as a service). The idea here is that the users do not need robotic expertise, do not require upfront capital, and need not worry about the risks of technological obsolescence and change. The RaaS model also fits into the operational budget of the users, further facilitating adoption. On the other hand, many follow a traditional model of equipment sales. Even these suppliers will also need to build in a subscription platform into their business model to offer maintenance and upgrades, especially cloud-based software updates. In other words, even these models will involve a large element of service revenue.

We assess that the market for such autonomous mobile robots (AMRs) will grow. There have also been some notable recent acquisitions. Amazon acquired a company focused on camera-based navigation, which would enable object detection and classification, and thus more intelligent navigation. Shopify acquired a firm with full solution including the entire software stack. This company also had RGB camera-based processing technology. The acquisition was at a very high multiple, but will give Shopfiy control over a full strategic technology essential in its recently-announced drive to diversify into the fulfilment business. Overall, our report "Mobile Robots, Autonomous Vehicles, and Drones in Logistics, Warehousing, and Delivery 2020-2040" forecasts that this will become a more than 200k robots could be sold within the 2020-2030 period (this figure includes those that can perform picking of regularly or irregularly shaped items). To learn more, please visit www.IDTechEx.com/Mobile.

Is the future of forklifts and tuggers autonomous?

The forklifts and tuggers are an indispensable tool in warehousing and logistics. They play numerous functions. Today, nearly all forklifts are manually operated. However, the rise of autonomous mobility technology will transform this trend. Indeed, the journey has already long begun. Many have developed, demonstrated, and deployed autonomous forklifts and trucks.

The left image panel shows from autonomous tuggers and forklifts from the following companies: SeeGrid, Geek Plus, Baylo, Vena Technologies, Kollmorgen, HIK Vision, AutoGuide (Teredyne), RoboCV, etc. The right chart shows our forecasts, in unit numbers, for autonomous forecasts. Note that these forecasts are long-term, covering the 2020-2040 period. The sale of such autonomous vehicles has increased in the past year or so. Nonetheless, we estimate the inflection point to occur around the 2025-2027 period. After this point, the market will very rapidly grow. To learn more, please visit www.IDTechEx.com/Mobile.

The choice of navigation technology is varied. Some use RGB camera and RGB image processing technologies to navigate. This field was extremely challenging in the past. Recent, deep learning advances however have seen this field completely transformed over the past 6-7 years or so. These strides now enable excellent localization and 2D object recognition, surpassing even human level capability. 3D object recognition errors rates are still high, but will rapidly evolve, especially with the use sensor fusion, e.g., ranging data from lidars. The camera-based technology will offer a more complete long-term roadmap towards improving the navigation. Many still utilize 2D lidar as it is easier to implement and is often good enough in known, controlled and slow-changing environment.

The cost of these forklifts is naturally higher, but the claimed ROI by many suppliers is within 12-18 months. The cost includes the installation and maintenance cost as well as the cost of the autonomous sensor suite, traction control and drivers, and the software, which can be amortized over a growing deployed fleet. Overall, price parity on an annual operational cost basis is nearly at hand in some high wage territories.

Over the past 1.5 years, this market has also entered into early stages of its growth phase. This trend is likely to continue and accelerate. The business scene is also very dynamics these days. For example, Teredyne acquired AutoGuide, enabling it to offer autonomous heavy-payload and large material handling and logistic vehicles such as tuggers and forklifts.

Our analysis and interview suggest that inflection point is likely to be reached around the 2025-2027. After this point, we project the sales to grow, already exceeding 100k units by 2030. Note that we generally develop 20-year forecasts for autonomous mobility as the technology will inevitably take time to be rolled out.

The report "Mobile Robots, Autonomous Vehicles, and Drones in Logistics, Warehousing, and Delivery 2020-2040" provides a comprehensive analysis of all the key players, technologies, and markets. It covers automated as well as autonomous carts and robots, automated goods-to-person robots, autonomous and collaborative robots, delivery robots, mobile picking robots, autonomous material handling vehicles such as tuggers and forklifts, autonomous trucks, vans, and last mile delivery robots and drones.