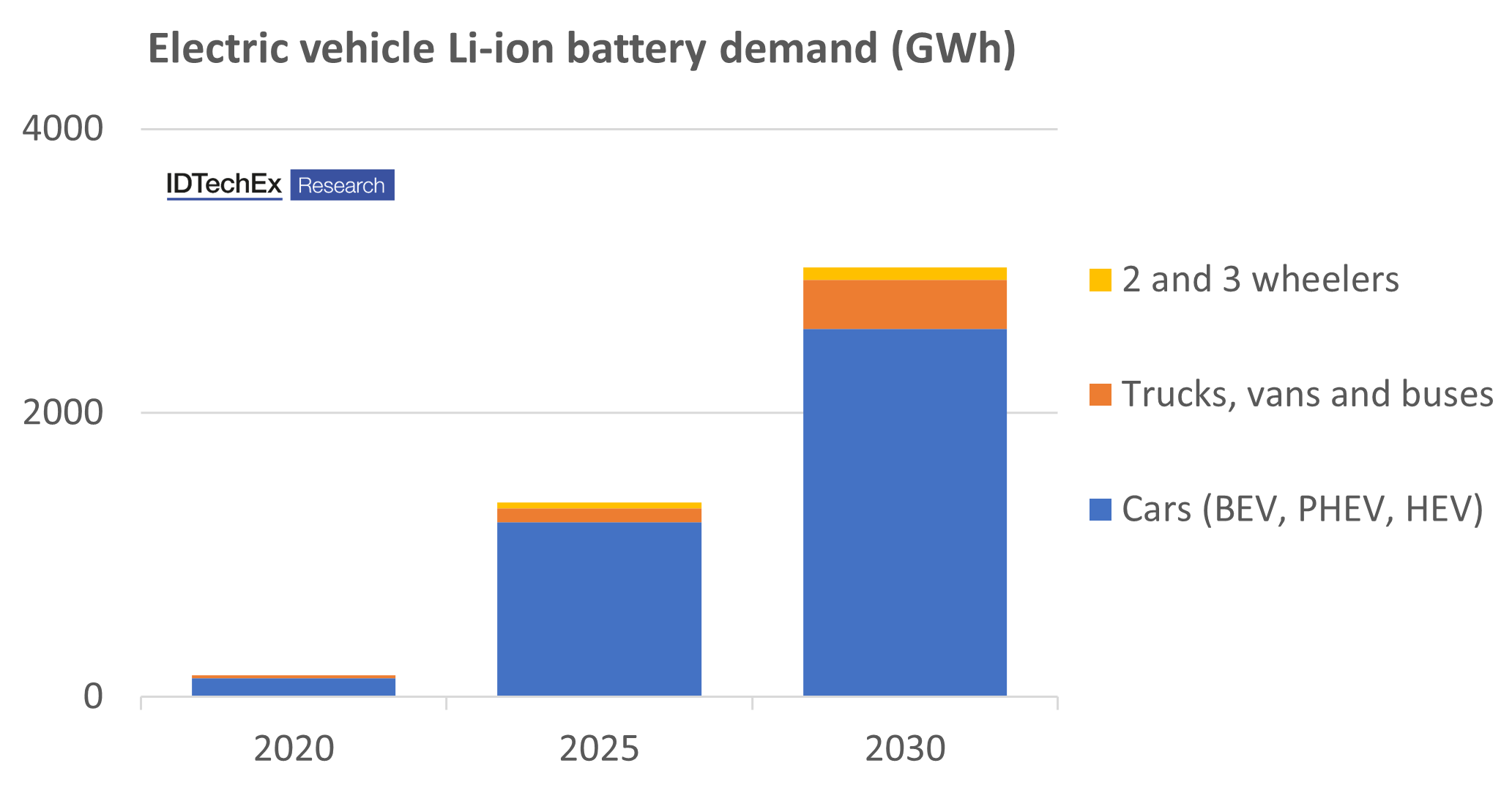

The global market for Li-ion batteries in electric vehicles is forecast to reach over US$380 billion by 2034, driven primarily by demand for battery electric cars but with rapid growth to other sectors too, including electric vans, trucks, buses, 2-wheelers, and off-road vehicles. Electrification and emissions targets, improving battery performance, and an increasingly attractive total cost of ownership for some vehicle segments are driving this growth in demand for battery electric vehicles (EV). Nevertheless, improvements to battery performance and cost are sought after and while developments may become increasingly incremental there are various avenues for the continued improvement of Li-ion battery technology.

The new research report from IDTechEx, "Li-ion Batteries and Battery Management Systems for Electric Vehicles 2024-2034", offers analysis of the technologies, designs and trends surrounding Li-ion cells, packs, and battery management systems (BMS), including Li-ion demand forecasts by EV application.

EV Li-ion demand growth. Source: IDTechEx.

Cells

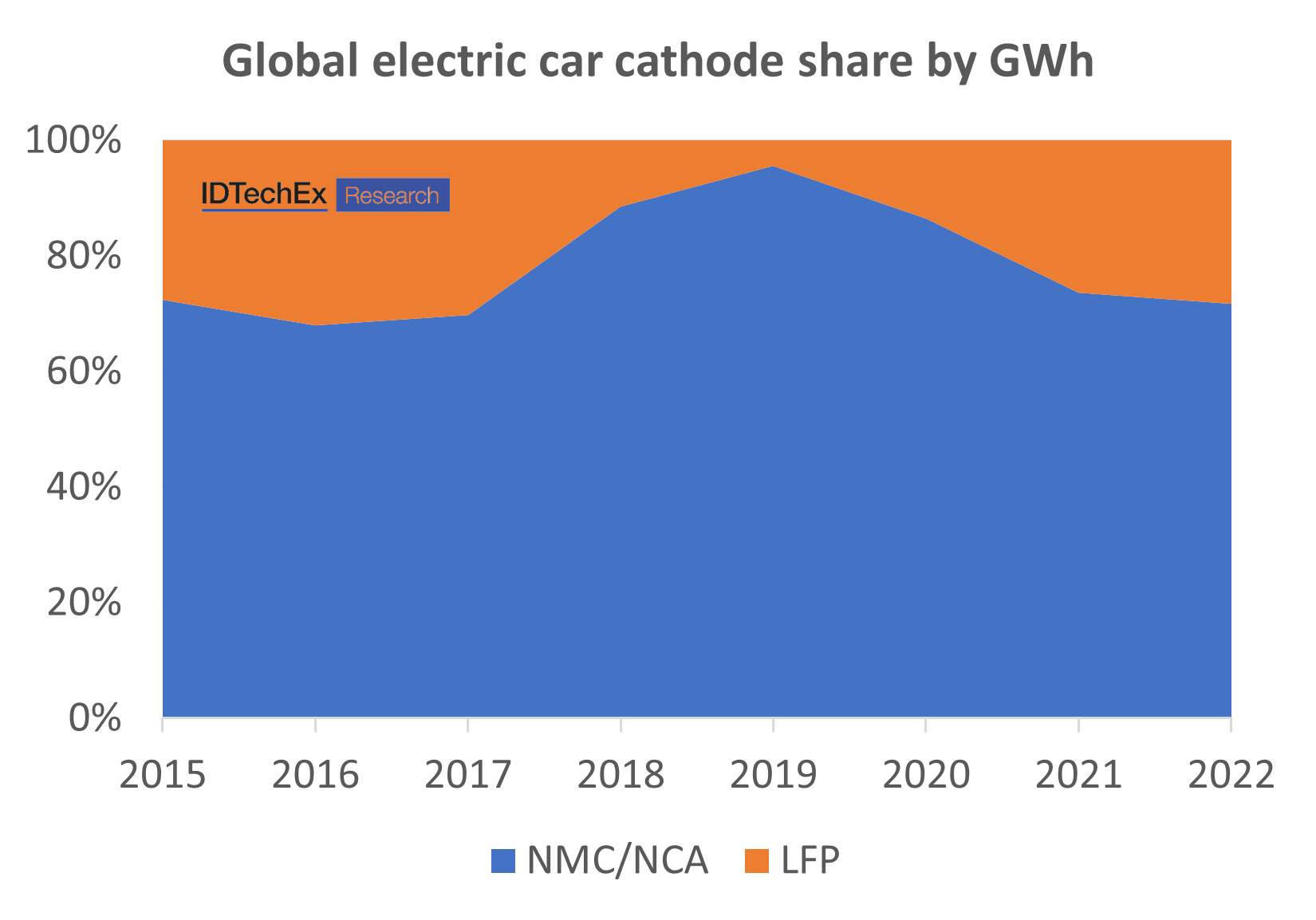

Over the short term, EV battery cells are likely to see a continuation of existing trends. For example, the average nickel content of NMC and NCA chemistries continues to increase as a means to increase energy density and reduce cobalt content. Possibly the largest trend is the general shift towards LFP, a cheaper and safer option than NMC and NCA (though not inherently safe). While the energy density of LFP can be 30-40% lower than NMC or NCA, the benefits of its lower cost have become unavoidable in recent years. As such, the share of LFP in electric cars has grown, though it needs to be noted that the vast majority of this has been driven by re-adoption in China. NMC and NCA are still favored in Europe and North America, though LFP has started to enter the market. NMC chemistries are also still favored in turnkey packs for other vehicle segments. Nevertheless, cost and material supply pressures, alongside technology improvements, mean LFP is forecast to grow its share of the EV market.

More transformative developments are also on the horizon. Announcements of solid-state battery developments continue while early commercialization is already taking place, for example, via the likes of Blue Solutions' polymer type solid-state batteries. The use of silicon anode material is expected to increase with the development of more advanced silicon anode solutions and commercially ready products, promising improvements to energy density and fast charging. New cathode chemistries continue to be explored too. For example, lithium manganese iron phosphate (LMFP) offers an interesting alternative with the potential to offer many of the benefits of LFP while increasing energy density closer to that of NMC type batteries, though commercial deployment is still limited.

Global cathode share in battery electric cars. Source: IDTechEx.

Pack Design

In light of the increasing LFP adoption within EVs, cell-to-pack battery designs take on added importance. These designs offer improved packing efficiency, increasing energy density to help reduce one of the primary disadvantages of using LFP versus NMC or NCA type batteries. CATL and BYD have implemented CTP designs alongside Tesla, Stellantis, and various other manufacturers. To improve gravimetric energy density, lightweight polymer battery enclosures are being pushed as an alternative to the incumbent steel and aluminum enclosures.

Dual-chemistry designs are also being explored by the likes of CATL, NIO, and Our Next Energy. Our Next Energy presents the most extreme example with plans to couple a high energy density but low cycle life chemistry as effectively a range extender LFP. Ultimately, combinations of different Li-ion chemistries, or even combining Li-ion with Na-ion, could help to optimize the inevitable trade-offs between power, energy density, cycle life and low temperature performance.

Thermal Management

Thermal management and fire protection have become critical considerations for EV batteries in light of safety concerns, high-profile fires, and battery recalls. While early electric vehicle models utilized passive air cooling, liquid cooling has become more prominent across various vehicle segments in recent years. According to IDTechEx data, active liquid-cooled designs made up 90% of the electric car market, compared to just over 50% in 2015. This trend applies not only to electric cars. Most turnkey batteries for commercial vehicle segments are offered with liquid cooling too. As developments in cell technology start to become increasingly incremental, developments in aspects such as thermal management become increasingly important to not only maintain safe operation but also maximize the available performance from Li-ion batteries.

Battery Management Systems

The battery management system (BMS) plays a critical role in the safe and reliable operation of any Li-ion battery. While the main functionality of a BMS is relatively well-defined, it also offers a route to expanding the performance envelope of Li-ion batteries. Improvements to safety, lifetime, fast charging, and even energy density are possible through developments to the BMS and, importantly, with minimal need to sacrifice one for another.

Critical to enabling the performance improvements is the development and implementation of more accurate battery and cell state estimation (e.g., state-of-charge, state-of-health, state-of-power), allowing the maximum performance to be safely extracted from a battery. Beyond developments to BMS software and algorithms, wireless BMS solutions are also being commercialized. By implementing wireless solutions, much of the wiring and cabling can be omitted, helping to reduce weight and eliminate potential failure modes. Though deployment is relatively slow, with GM's initial announcement for their wireless BMS in 2020, BMS semiconductor manufacturers are now offering solutions for wireless BMS designs.

The new IDTechEx report, "Li-ion Batteries and Battery Management Systems for Electric Vehicles 2024-2034", provides analysis on key innovations, advancements and trends in li-ion batteries and BMS in EVs, including discussion of performance data. The report provides an overview of some of the key drivers, challenges and battery technology choices for multiple electric vehicle segments. For more information, including downloadable sample pages, please visit www.IDTechEx.com/EVLithium. To see IDTechEx's wider portfolio on the Li-ion and electric vehicle sectors, please visit www.IDTechEx.com/Energy.

IDTechEx guides your strategic business decisions through its Research, Subscription and Consultancy products, helping you profit from emerging technologies. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.