The supercapacitor industry closed last year (2013) with a continued double-digit growth. According to Maxwell Technologies' executives, China has been the main source of growth. New announcements confirm what IDTechEx has stated in recent years: the supercapacitor and the battery industry are the same. You will learn why in our report Supercapacitor / Ultracapacitor Interviews, Strategies, Road Map 2014-2025 or by attending our forthcoming event Supercapacitors Europe, 1-2 April in Berlin.

An example of this is a recent announcement by Maxwell Technologies about the signature of a memorandum of understanding to develop "next generation energy storage solutions leveraging the complementary characteristics of SK's lithium ion batteries and Maxwell's ultracapacitors". This could mean that they will either develop hybrid supercapacitors, meaning by this a device with an electrode of a lithium battery and an electrode of a supercapacitor, or they will integrate supercapacitors to protect batteries (as coupled but separate devices) in different applications. At the recent IDTechEx event, Supercapacitors USA 2013, Maxwell showcased how supercapacitors can actually extend the lifetime of batteries 1. This memorandum of understanding could mean to follow up on this route. In late 2012 when IDTechEx asked Maxwell Technologies' Jeremy Cowperthwaite whether they were working on hybrid technologies, the answer was that they were working on what they think will be the next generation of ultracapacitor technology that will provide increased energy density, but that it was a different path and different from asymmetric (hybrid) technology. However, it seems that this recent announcement is heading in the hybrid device direction based on SK Innovations comment: "As our name implies, we are seeking to move beyond the limitations of existing technologies to develop and deliver products that better meet the requirements of the most demanding energy storage and power delivery applications," said Stephen J. Kim of SK Innovation's battery division.

On another topic, 2013 finally saw the kick-off of sales in electric cars and the new impetus on fuel cell cars. It seems that the usual suspects of the oil and gas sector are not willing to let electric cars win the challenge of the green car of the future so easily. This is because, against the background of contentious debates on the two sides of the Atlantic (i.e. Canada2 and the UK3) in relation to the environmental impact of shale gas production, hydrogen fuel cells cars are being seen (once again) with a 'new hope'. Companies like Toyota, GM and Daimler supported by obvious interested parties, like Shell and Total, have announced the launch of their fuel cell models in California in 2015 (Toyota) however other companies such as Volkswagen have stated that they do not see a future of hydrogen fuel cell cars at all. And when we were thinking that Germans were blunt, Tesla's CEO Elon Musk did his own comment on his own terms: "Hydrogen fuel cell cars are bullshit". On more moderate terms, Carlos Ghosn, Nissan's CEO, is backing Tesla's position. Ghosn said he thinks the technology for hydrogen-powered cars won't be ready until at least 2020 but he believes that electric cars are going to the major component of the car industry.

There are technological and strategic reasons behind this difference of opinion. Paying attention to who says what, it is important to consider the different market positions of each player. Neither Toyota nor Daimler can claim to be the world's main car producer; that position belongs now to Volkswagen (2012 figures) and in addition it is the best car seller in China (2013 figures). This is relevant because the automotive industry is slowly recovering from the economic recession and China is today the highest growth and largest car market in the world. Volkswagen's market share is considerable in China because it is 3.3 million units ahead of his closest competitor, General Motors. Japanese companies are not taking part in this growth. The current state of Sino-Japanese relations deteriorated with a recent visit to Yasukuni Shrine by Japanese Prime Minister Shinzo Abe. This is not making things easier for Akio Toyoda, Toyota's CEO, who previously indicated that the company's sales in China would continue to be overshadowed by the poor Sino-Japanese relationship4. An additional explanation about different positions on automotive power trains is related with energy resources. Specifically we may ask, what is behind the launch of the fuel cells car in the USA? Well perhaps it is related to the fact that 39% of the shale gas was produced there against China's 1% in 2013 according to US DOE5. On the technological side, we all know currently most of the hydrogen comes from fossil fuels (natural gas reforming) so in order to have a claim as a green vehicle it would have to be produced by an alternative clean route.

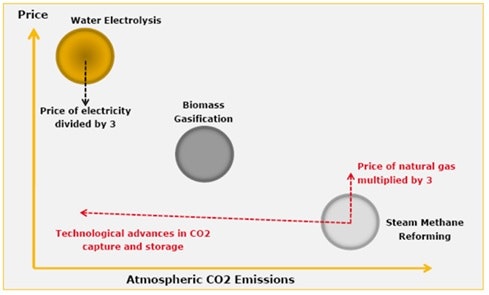

Fig. 1. Different processes and challenges

Source: IDTechEx

As explained in IDTechEx's report, Hydrogen and Fuel Cells 2014-2025: Forecasts, Technologies and Markets three options are in the landscape. The first is biomass gasification, which in turn could come from either biofuels or waste. Biofuels have recently have been a quite polemic options since a recent detailed study by a recognized institution6 mentioned that in addition to the serious indirect consequences of biofuels they would only postpone global warming by 58 hours! It is alarming to mention that the support for biofuels costs taxpayers in Europe £6 billion/year. Waste is a more sensitive option, but can we run all our automotive fuel demands on waste? BMW is working on the 'Landfill Gas-to-Hydrogen' project, whilst less CO2 intensive it is still not totally a zero carbon solution since still uses steam methane reforming. This last option could be coupled with capturing and storing CO2 emissions from hydrogen production from fossil fuels (known as CCS), whilst carbon capture is a portfolio of technologies already known, its last chain, the storage is actually still not very well understood. This has been evidenced by recognised British geologists such as Brian Lovell7. Finally, there is water electrolysis based on renewable energy, which is truly a clean source of hydrogen but unfortunately still terribly inefficient, since the well to wheel efficiency of fuel cell cars is just 25% which is poor compared with 50% of electric cars in the same energy conversion path.

Electricity expense constitutes the largest fraction of hydrogen production costs and high hydrogen production expenses count as the main deficiency of commercial and industrial electrolysers. Hence electrolytic methods are usually outperformed by other approaches such as steam methane reformation. Fuel cells themselves still need to reduce their cost; this is even considering that they have already reduced their price from 1 million usd to 100,000 usd. Finally the investment of one hydrogen charging station equals six electric fast charging stations. For all these reasons hydrogen fuel cell cars still have a long way to catch up in all dimensions to compete for mass adoption.

Whether it is hydrogen fuel cells or batteries, both will perform better with supercapacitors, because neither fuel cells or batteries can cope with high power surges (i.e. acceleration) and if they are exposed to them (which is desirable by most drivers) they will reduce their operational lifetime. Let's not forget that batteries and fuel cells account for more than 50% of the cost of both fuel cell and electric cars. IDTechEx has raised this point since our first Supercapacitor conference when showcasing the Riversimple fuel cell electric car at our conference in Washington in 2012. At Supercapacitors Europe 2014 we will have a follow up in the topic with Imperial College's Dr. Billy Wu speaking about 'Supercapacitors as Fuel Cell Life Extenders'. Dr. Andrew Burke from UC Davis will speak about its recent performance tests of the supercapacitors available in the industry, so if you want to learn what you need to know when selecting a supercapacitor this is the session to follow. On the industry side, Cap-XX from Australia will present their most recent developments and Skeleton Technologies (one of the few European supercapacitor companies) will speak about their new activities in Germany. Other speakers include Jari Keskinen from VTT Technical Research Centre Finland speaking about printed supercapacitors, Teresa Centeno from Spain's Institute Nacional del Carbon, will speak about carbons in supercapacitors - characteristics and performance, and finally with a very interesting topic, Dr. Antonio Varzi, from the University of Munster, will speak about green binders in supercapacitors.

IDTechEx's Supercapacitors Europe 2014 event is the place to be to learn about the new emerging energy storage industry. Join us on the 1-2 April in Berlin - www.IDTechEx.com/SCEurope

7 Challenged by Carbon, Bryan Lovell